Wealth Unbound

Most successful entrepreneurs are sitting on a gold mine—and they don’t even realize they’re trapped in it. You’ve built a business that generates millions in revenue. You’ve got the team, the clients, the lifestyle. Maybe you even own the building, drive the truck you bought through the company, or pull a healthy six-figure income. But here’s the uncomfortable truth: If 80–90% of your wealth lives inside your business, you’re not wealthy—you’re vulnerable. The Illusion of Success On paper, everything looks great. You have a business valued at $5M, $10M, maybe even more. But try to access that wealth today—without selling the company—and you’ll quickly realize it’s not liquid, diversified, or protected. Your business is your biggest investment and your biggest liability. When the economy shifts, your valuation can drop overnight. When a key employee leaves, profits tighten. When taxes or debt pile up, your flexibility disappears. And yet, most business owners stay in the cycle—pouring every ounce of profit back into the company, hoping it will someday “all pay off.” That’s The Trap: the illusion that business success automatically equals personal wealth. The Three Signs You’re Caught in The Trap Concentration Risk – Your net worth is tied to one asset: your business. If something happens to it, your family’s wealth, income, and future all move in the same direction—down. Tax Drag – You’re paying top-bracket taxes on business income without a coordinated wealth strategy. You may be losing 30–40% of potential wealth every year simply because you haven’t structured things tax-efficiently. Exit Uncertainty – You tell yourself you’ll sell “someday,” but there’s no timeline, plan, or buyer strategy. The business might be sellable—but not transferable. And without systems and recurring revenue, your valuation may not be what you think. Measuring What Actually Matters: The Profit-to-Wealth™ Scorecard We created the Profit-to-Wealth™ Scorecard as a diagnostic tool for business owners who want to measure what truly matters: how effectively you’re converting your business profits into personal wealth. It’s not about revenue. It’s not about valuation. It’s about transferable wealth readiness. The Scorecard measures five key areas: Profit Structure – How predictable and margin-efficient is your business? Tax Efficiency – How much of your earnings stay with you after taxes? Liquidity & Diversification – How much wealth exists outside the business? Exit Readiness – Could your business run—or sell—without you? Freedom Alignment – Are your finances aligned with the life and legacy you want to live now? When scored honestly, most business owners discover they’re only operating at 40–60% of their potential. That means half of their wealth is still stuck inside the business—unrealized, unprotected, and untapped. Breaking Free from The Trap The goal isn’t to abandon your business. It’s to use it as the engine that funds lasting, transferable wealth. That means shifting from: Reactive profits → to intentional wealth creation Tax payments → to tax strategy Owner dependency → to transferable value It’s not about working harder. It’s about working smarter with what you’ve already built. Take the First Step If you suspect you’re caught in The Trap, start by finding out where you stand. Take the free Profit-to-Wealth™ Scorecard and see your business wealth readiness score. It only takes five minutes—and it could change how you think about success forever. 👉 Take the Scorecard Assessment→ https://www.unboundcapitaladvisors.com/profit-to-wealth-assessment (Link to your live form or Duda page) Because your business was never meant to be your prison. It was meant to be your path to freedom.

💡 Introduction For most business owners, taxes are the single biggest expense. Yet many owners unknowingly overpay every year because their tax strategy is reactive, not proactive. By using proven strategies, entrepreneurs can free up significant cash flow — money that can be reinvested, used for liquidity, or saved for future exit planning. Here are five tax strategies every $2M+ business owner should know. 1️⃣ Optimize Entity Structure 🏢 Choosing between S-Corp, C-Corp, or LLC can save tens of thousands each year. The wrong structure = unnecessary payroll or double taxation. 2️⃣ Strategic Owner Compensation 👔 Balancing salary and distributions minimizes payroll tax while keeping the IRS satisfied. Done wrong, this mistake alone can cost six figures over time. 3️⃣ Advanced Retirement Plans 📈 Standard 401(k)s cap out quickly. Cash balance and defined benefit plans allow contributions of $100K–$250K+, creating huge deductions for owners. 4️⃣ R&D and Other Credits 💡 Even service companies may qualify for credits like the R&D Tax Credit. Bonus depreciation and Section 199A deductions can add up quickly. 5️⃣ Exit Planning Ahead of Time 🚪 If you’re planning to sell in 3–5 years, set up strategies now: QSBS exclusion, charitable trusts, and installment sales can save millions at exit. ✅ Next Step Tax savings aren’t just about this year’s return — they’re about unlocking liquidity and building wealth for decades. At Unbound Capital Advisors, we specialize in helping $2M+ business owners reduce taxes, create liquidity, and prepare for their best exit. 👉 Schedule your Business Owner Strategy Session today and start keeping more of what you earn.

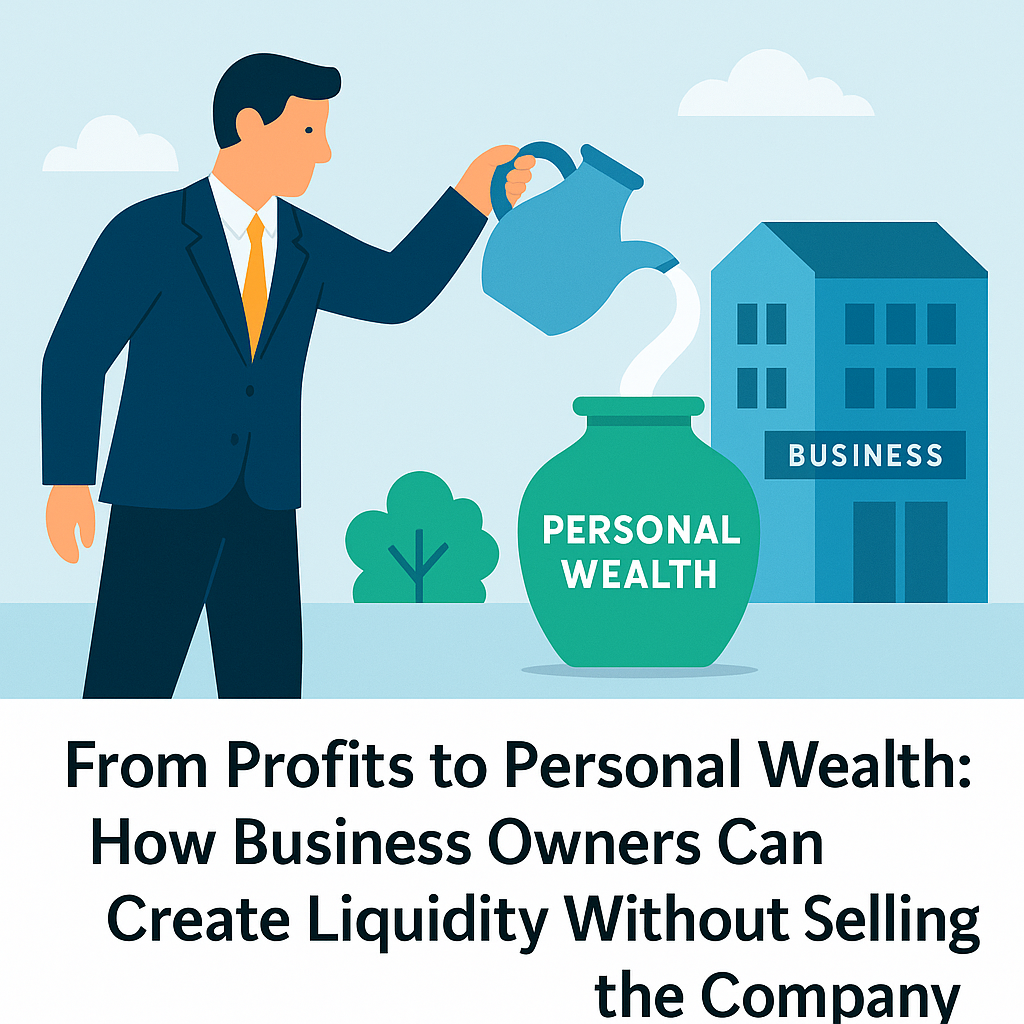

💡 Introduction For many business owners, most wealth is tied up in the business itself. On paper, you may look successful — but when it comes to personal liquidity, things can feel tight. Relying entirely on the company creates risk: what happens if growth slows, or if you face an unexpected downturn? The good news: you don’t need to sell your company to create financial freedom. By taking intentional steps, you can pull liquidity out of your business while still running it. 💧 Why Liquidity Matters Reduces concentration risk (all your wealth tied to one asset). Creates personal safety nets for you and your family. Provides capital for outside investments. Strengthens your negotiating position in a future exit. 🔑 Strategies to Build Liquidity Without Selling Owner Compensation Review → Balance salary, dividends, and distributions to optimize tax efficiency and take home more cash. Tax-Advantaged Retirement Plans → Cash balance or defined benefit plans allow six-figure contributions while reducing current tax burdens. Debt Restructuring → Smartly leveraging debt can free up cash flow for personal wealth building. Partial Recapitalization → Work with investors or lenders to take chips off the table while keeping control. Systematic Profit Allocation → Commit a percentage of profits to flow directly into a personal portfolio outside the business. ✅ Next Step Liquidity isn’t about taking money away from your business — it’s about protecting yourself and your family. At Unbound Capital Advisors, we help owners design strategies that balance business growth with personal freedom. 👉 Schedule your Business Owner Strategy Session today and learn how to unlock wealth without waiting for an exit.

For many business owners, the company isn’t just their livelihood — it’s their life’s work and their largest financial asset. Yet too often, owners wait until they’re “ready to sell” before thinking seriously about an exit. By then, most of the best opportunities to save taxes, increase valuation, and protect their wealth are gone. The result? Lost millions in avoidable costs. Here’s why waiting too long to plan your exit is a mistake — and what you can do now to avoid it. ⏳ Exit Planning Is a Process, Not an Event Too many entrepreneurs think of exit as a transaction — one day they’ll sell, transfer to family, or hand the reins to management. In reality, exit planning is a multi-year process that involves: Valuation → Understanding what your business is worth today Preparation → Fixing risks, improving financials, and strengthening systems Transition → Identifying the right buyer or succession strategy Legacy → Aligning wealth with your family and purpose Waiting until the last minute skips steps 1–3 — often leading to discounted value and higher taxes. 💸 The Hidden Tax Bill When you sell your business, taxes can consume 30–40% of the proceeds. With proper planning — using strategies like QSBS exclusions, charitable trusts, or installment sales — you could preserve millions. But most of these tools need to be set up years before an exit to be effective. If you wait until closing day, it’s simply too late. 📉 The Impact on Valuation Buyers pay a premium for companies that are: Well-documented Systematized (not dependent on the owner) Clean in financials and structure Owners who rush into a sale without preparation often face “haircuts” on valuation — leaving 10–20% of potential value on the table. On a $5M sale, that’s $500K–$1M lost just from poor prep. 🚀 The Freedom of Early Planning Planning early isn’t just about numbers. It’s about peace of mind: Knowing your family is protected if something happens to you Creating personal liquidity before an exit Having time to align your wealth with your long-term purpose The sooner you start, the more options you have — and the more wealth you’ll keep. ✅ Your Next Step At Unbound Capital Advisors, we specialize in helping business owners: Reduce taxes before exit Create liquidity outside the business Design succession and legacy strategies Don’t wait until you’re ready to sell. The best exits start 3–5 years in advance. 👉 Schedule your Business Owner Strategy Session today and take the first step toward a profitable, stress-free transition.

Discover the 5 biggest mistakes business owners make when planning an exit or liquidity event—and how to keep more of your hard-earned wealth.

As a business owner, you know how important margins are. You work hard to protect profits, manage expenses, and reinvest into growth. Yet, when it comes to building wealth outside your company, many owners unknowingly let fees erode their financial future. These costs often hide in plain sight — small percentages that seem harmless at first glance — but over time, they snowball into six- or even seven-figure losses. 💸 Why Fees Matter More for Business Owners Business owners often delay personal investing because so much capital is tied up in the company. When you do build liquidity outside the business, every dollar has to work as hard as possible. But fees — whether from advisors, funds, or hidden costs — quietly drag down returns. The dollars you’re losing to fees aren’t just gone today; they’re dollars that could have compounded for years and supported your eventual exit, succession, or retirement. Example: If you invest $1M from a partial business sale and pay a 1% annual fee, that’s $10,000 per year. Over 20 years, that “small” fee could cost you more than $400,000 in lost growth. ⚠️ Common Fee Traps for Business Owners 🏦 Asset-Based Advisor Fees (AUM) Many advisors charge 1%+ of assets each year. As your liquidity grows after an exit or sale, so does their fee — regardless of the value they deliver. 📊 Mutual Fund & ETF Expense Ratios Actively managed funds often hide higher fees in “expense ratios,” eating into returns. Lower-cost index funds or ETFs can keep more in your pocket. 🔄 Trading Costs & Turnover Advisors chasing short-term gains can rack up commissions and taxable events. Business owners especially need stability and tax efficiency. 📑 Hidden Costs & Fine Print 12b-1 fees, sales loads, and maintenance charges may look small but add up quickly — and rarely provide real value. 🧾 The True Cost of “Just 1%” The math doesn’t lie: A $1M portfolio growing at 7% with a 1% fee → $3.8M in 30 years. The same portfolio with a 0.25% fee → $4.8M in 30 years. That’s a $1M difference, purely from fees — not performance. For business owners, that difference could mean the ability to: Retire earlier Fund a smoother succession plan Give generously to causes that matter ✅ How to Protect Yourself Know What You’re Paying Review your investment accounts and advisory agreements for all costs. Choose Transparent Pricing Avoid percentage-based AUM fees. Look for flat-fee advisors who align incentives with you, not your portfolio size. Favor Low-Cost Investments Index funds and ETFs often outperform after fees compared to high-cost funds. Simplify Consolidate accounts to reduce overlapping charges and complexity. 🔑 The Unbound Capital Difference At Unbound Capital Advisors, we’ve seen firsthand how fees quietly drain business owners’ wealth. That’s why we use a flat-fee model — no AUM skim, no commissions. Our mission is simple: Help you reduce taxes and protect cash flow Build liquidity outside the business Prepare for a profitable exit and lasting legacy So every dollar works as hard for your personal wealth as it does in your business. 👉 Ready to see how much you could save? Schedule a free Business Owner Strategy Session today or download our Exit & Liquidity Guide to start building wealth unbound.